Copy Link

Copy Link

E-mail

E-mail

LinkedIn

LinkedIn

Facebook

Facebook

Telegram

Telegram

WhatsApp

WhatsApp

Latest Updates

Experiential Innovation for Bankers

Does a Good Customer Experience Guarantee a Strong Customer Relationship?

Unfortunately, it does not! In fact, the strength of customer relationships depends much more on the consistency of experiences and their correlation with the expectations of the customer. As well, the strength of customer relationships tends to be based much more on the emotional side of customer contacts than the rational. Because of this, we spent the last couple of years adding some structure to the connection between individual customer experiences and the resulting relationships that may or may not evolve from those individual contacts.

To start with, we studied everything we could find on the topics of customer experience, customer relationships, and loyalty: books, articles, white papers, research findings, blogs, and thought leadership pieces from various authors, consultancies, and research firms. We studied up on service quality, sales force effectiveness, operational excellence, segmentation, innovation, customer experience, loyalty, etc. and everyone seems to agree that the relationship with the customer will be of the utmost importance for the future of any bank. In fact, Mc Kinsey & Company states in their publication, The Future of Retail Banking, that the successful banks of the future will “excel at building and leveraging customer relationships”. [1] The report from Deloitte titled Rebuilding the Relationship Bank states that banks “need to build stronger customer relationships”. [2] Bain & Company, Inc. states in a recent report that based on the regulatory difficulties that banks face, “the best way forward will be organic growth rooted in strong customer relationships”. [3] Ernst & Young states that “it is more critical than ever that institutions maintain strong relationships with their customers” [4] in the 2011 release of their Global Consumer Banking Survey.

This is not a new trend. The buzz around customer relationships has been going on for years. We even found a book written by Stefan Kaminsky and published Michael Lafferty in 1989, Beyond Retail Banking: How to Keep Your Customers Happy and Loyal – Forever!, that outlines the need for a closer relationship with customers and the importance of value added activities such as giving people sound financial advice. It seems that not many would disagree that the relationship between bank and customer is important; however, Mc Kinsey & Company also states in their report, specifically in the section entitled “Back to the Future: Rebuilding the Relationship Bank” that only a few banks “have taken initial steps toward developing a full customer relationship view – let alone incorporated it into their sales, service, and risk strategies.” [5]

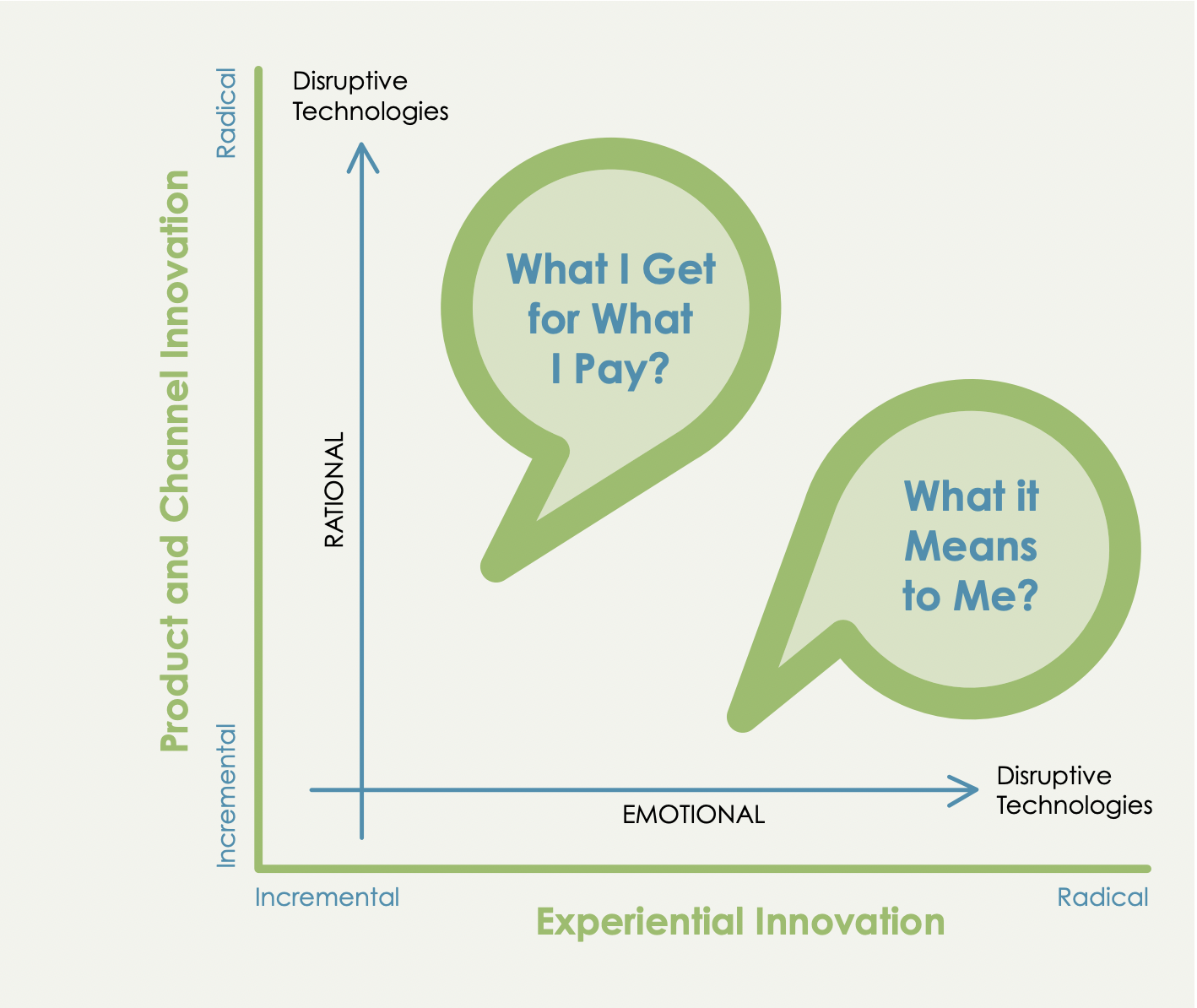

The problem seems to be that no one has really agreed on what the relationship is or can be outside of selling and servicing (or from the customer’s point of view: purchasing and using), which doesn’t necessarily fulfill the dynamic of a healthy relationship (as outlined in the article: The Relationship-Centric Bank. Possibly, the problem is the result of the type of innovation in banking over the past decade, which has mainly been focused on technologies that enhance the products a bank offers or technologies that create easier (lower cost) methods for customers to access the functionality of those banking products. Considering these innovations, some brought incremental improvements while others brought radical changes. Those more radical changes (internet banking, mobile banking, etc.) were, in essence, market-changing technologies for the banking industry.

All the way back in 1995 in their paper Disruptive Technologies: Catching the Wave, Clayton Christensen and Joseph Bower outlined the concept of disruptive technologies as market-changing technologies that have the potential to revolutionize an industry. [6] There have been a few of those in banking over the past decade, but most have been either related to the functionality or characteristics of products that banks offer or the channels through which customers access those products. And much of the focus for these innovations was an effort to increase efficiency by improving operational throughput, improving risk management or lowering the cost of contacts with customers.

These innovations may have accomplished the task of higher efficiency and lower cost, but because a significant portion of these innovations fall into the category of self-service and remote self-service channels, in effect, they made the relationship with the banks more distant. In response, a wave of innovation started related to the softer side of banking in an effort to “re-connect” with customers. We refer to this as Experiential Innovation which is related to the more emotional and sensory side of the relationship.

If we take a look at these two types of innovation, the Product and Channel innovation, for the most part, represents the rational aspects of the customer relationship: What a customer receives in exchange for payment (how they access the products they own, what functionality exists in those products, and how easy it is to use the products). Whereas, the emotional side exists in Experiential Innovation: how the customers feel about the relationship and what it means to them.

Over the past decade, the complexity of product and channel innovations has increased and the speed at which competitors can copy those innovations has also increased.Ten to fifteen years ago, it was much easier to be the first bank with XYZ new product or the first bank with ABC new channel, and the competitive advantage and price premium lasted for much longer. Today, there is much more complexity in generating a new disruptive technology, and the time that the bank may enjoy a competitive advantage or price premium is much shorter. As a result of this, and the desire to reconnect with customers, we have seen a shift in the attention of banks to Experiential Innovation in its most basic forms – mainly how to make sales more effective and service more pleasing.

If banks want to play a significant role in the lives of their customers, they will have to help customers along the path of realizing their goals, dreams, and aspirations.

For the past 5-7 years, we have increasingly seen banks dabbling in this concept of Experiential Innovation, mainly in their communications and in their physical points of presence – their branches. There have been many examples: Washington Mutual Occasio Branches [7]; Deutsche Bank of the Future (Q110) [8], ABN-AMRO Financial Centers [9], Jyske Bank Branches [10], ING Direct Cafés [11], Umqua’s Community Centers [12], etc. There have been many examples of experiential twists to the physical banking environment, but they have not radically changed the way that customers feel about the banking relationship and what it means to them. Even Sberbank (Russia’s largest bank with about 60% market share in deposits) has recently launched a Branch of the Future. [13] We have seen some very cool and innovative things in and around bank branches in the last few years that we wouldn’t normally expect from bankers, such as:

- Branch sound systems with different content schedules in different zones and the use of sound domes and Panphonic Sound Signs to isolate sound to specific small areas.

- Digital merchandising systems with local messaging and information, touch screen video walls interactive projection walls, and video façades

- Coffee, cookies, candies, popcorn, and even water bowls and dog biscuits for people that bring their dogs into the branch

- Lifestyle and life stage themed product packages and zones in branches

- Kids play areas complete with Playstations and Wii game consoles, lego play tables, clowns

- Touch screen tables and kiosks with interactive content and streaming video and even internet café areas

- Smell generators capable of generating different smells in different zones and at different times.

- Beautiful, innovative, even futuristic design of the environment and communications

- Experiential (sometimes even controversial) communications such as human billboards, random acts of kindness / convenience, WooHoo moments.

This list is just the beginning of the many variations of experiential innovation that we have seen, but, still, most of the experiential innovations to date have been designed to engage the senses and generate emotions “in the moment” of contact. This is a good start. Making individual contacts more pleasing from a sensory and emotional standpoint is a huge step in the right direction. However, we still have not seen a significant effect in the way that customers feel about their relationship with the bank or the overall value of the relationship for customers. As well, bankers have not seen the wave of new clients or the profitability that they expected from the costly inclusion of these elements in their budgets. In fact, many of the innovations listed above have not been implemented across all branches of a bank’s network. Chase has completely refurbished the Occasio branches that it inherited in the Wamu network, [14] Deutsche Bank has not rolled-out the Q110 concept in its entirety, and others simply have not seen the “bang for the buck” that they expected. Is the experiential side of banking really the future, or should we all just go back to good service / low price?

Disruptive Relationships

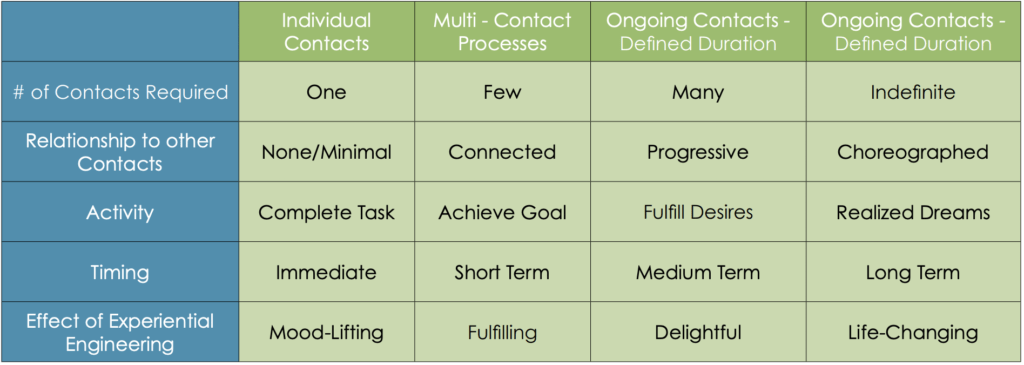

Is it possible that banks have missed the point when it comes to experiential innovations? Bower and Christensen state that disruptive innovation often “sacrifices performance along dimensions that are important to current customers and offers a very different package of attributes that are not (yet) valued by those customers. At the same time, the new attributes can open up entirely new markets.” [15] But finding the next new disruptive technology in banking represents an increasingly difficult task and, visibly, one that does not guarantee long-lasting rewards. What is the new or different package of attributes that a bank can offer to customers? One path is further product and channel innovation trying to find the next, new disruptive technology. The other is to seek more radical changes in the area of experiential innovation. So far, we have seen some incremental improvements to the emotional and sensory aspects of contacts with the bank. We have seen some flashy technology and gimmicky tactics along with some things that take the seriousness away from banking like Wamu’s WooHoo Moment. [16] But these are not radical changes in the emotional side of banking, and very few have a clear idea of how these radical changes might materialize. If we take a look at the trajectory moving from incremental improvements to radical change in the area of experiential innovation, we can find quite a bit of guidance. In general, the majority of experiential innovations that we have seen so far have been related to improving the quality of individual contacts using emotional and sensory stimulation. In some cases, we have seen enhancements to multi-contact processes, such as sales processes for more complex product categories, but most of the improvements we have seen remain “in the moment”- only answering the needs of today and not considering the potential of the ongoing relationship.

Over the past decade, the complexity of product and channel innovations has increased and the speed at which competitors can copy those innovations has also increased.Ten to fifteen years ago, it was much easier to be the first bank with XYZ new product or the first bank with ABC new channel, and the competitive advantage and price premium lasted for much longer. Today, there is much more complexity in generating a new disruptive technology, and the time that the bank may enjoy a competitive advantage or price premium is much shorter. As a result of this, and the desire to reconnect with customers, we have seen a shift in the attention of banks to Experiential Innovation in its most basic forms – mainly how to make sales more effective and service more pleasing.

Considering the nature of the relationship between bank and customer, the bank is almost guaranteed a regular opportunity to enhance the experience of the overall relationship as well as the individual contacts. In fact, any relationship is essentially the collection of contacts between the two parties over time. As such, each individual contact should be positive, engaging, and fulfilling. But also, the result of the collection of those contacts should also be positive, engaging, and fulfilling. Here we return to the question of what customers seek from a bank relationship and the progression and growth of that relationship over time. As outlined in the article: The Relationship-Centric Bank, most customers when asked today state that they want “good service at a low price” from their bank, but when asked what they hope to receive from their banking relationship over the course of 5-10 years, they answer on a much more transformational level: “help when I have a problem”, “help managing my day-today financial issues”, “help realizing goals and dreams”.

If banks wish seize the opportunity to play a significant role in the lives of their customers, they will have to engineer more than individual contacts with experiential components. The overall relationship will need to be engineered (even choreographed) to generate a positive, engaging, and fulfilling result in the lives of the customers – in effect, helping customers along the path of realizing their goals, dreams, and aspirations.

Fulfilling this component represents the ultimate level of experiential innovation – moving from incremental improvements (engineering individual contacts to be experiential in terms of emotional and sensory stimulation) to radical improvements (engineering an ongoing collection of contacts to help guide the growth and transformation that people seek in their lives). If the result of product and channel innovation is more rational value received by the customer (convenience, speed, functionality, ease of use, etc.), the result of the experiential innovation is the emotional value received by the customer. The effect of experiential engineering related to each individual contact (how a person feels about the contact) has the potential to be mood-lifting, but engineering a collection of contacts so that the customer finds meaning and direction in the relationship has the potential to be life-changing. The individual contact may help the customer to complete a task in the immediate term; whereas, a well choreographed set of contacts over time could help customers to realize their dreams in the long-term.

As well, moving from incremental improvements to radical improvements in the realm of Experiential Innovation requires a new set of processes and measures that will allow bankers to see their customers lives as more than a simple set of unrelated contacts. Properly implemented, this approach has the potential to create Disruptive Relationships, developed over time as the result of the positive, engaging, and fulfilling collection of contacts with the bank that help the customer to achieve their aspirations. Joe Pine, co-author of The Experience Economy, recently wrote about “learning relationships” in an article called Beyond “Products & Services” in Banking. He describes that learning relationships with customers would give bankers the ability not only to provide individual solutions, but to guide transformations in the lives of customer by using numerous solutions at different points in the relationship through their knowledge of the customer’s individual needs, wants, desires, and dreams.

It seems that the sweet spot for bankers will be in finding a cost balanced format in which they can engage both the emotional and the rational aspects of their customers’ lives. In reality, banks are not the most engaging organizations around, but they do have the ability to significantly influence a customer’s quality of life and their ability to realize their goals and dreams. Finding this balance of emotional and rational, versus resigning themselves to the inevitable continued commoditization of their industry, should be on the top of every banker’s agenda.

[1] “The Future of Retail Banking”, McKinsey & Company Financial Services Practice Report (November 2010), 2

[2] Rebuilding the Relationship Bank Delivering a Complete Customer Experience”, Deloitte Center of Banking Solutions report (May 2009)

[3] “Customer Loyalty in Retail Banking North America 2010”, Bain & Company report (2010), 1

[4] “A New Era of Customer Expectation Global Consumer Banking Survey 2011”, Ernst & Young report (2011), 13

[5] “Future of Retail Banking”, McKinsey & Company, 56

[6] Joseph L. Bower and Clayton M. Christensen,“Disruptive Technologies Catching the Wave”, Harvard Business Review January-February 1995

[7] William B. King, “Building the Great Retail Bank: Who’s Doing it Right,” Bank Director Magazine, 4th Quarter 2004

[8] “Q110: Deutsche Bank of the Future”

[9] “The Future Role of the ‘Bank Store’ and its Interconnectivity with Other Channels”, A report by the EFMA Banking Advisory Council in partnership with Microsoft (2007), 25

[10] “The Danish Branch is Beyond Cool”, October 28, 2008

[11] “Free Tour of all 11 ING Direct Cafes in North America”, November 8, 2010

[12] Laura Gunderson, “Latest Umpqua ‘Store’ Alters Banking Experience”, May 19, 2010

[13] “Sberbank’s Branch of the Future”, December 18, 2009

[14] Michael Sisk, “The Future of the Bank Branch”, Bank Technology News, July 2009

[15] Bower & Christensen, “Disruptive Technologies Catching the Wave”, 1

[16] Eric Newman, “WaMu Wants Customers Yelling Whoo-Hoo”, February 13, 2008

The best article in your inbox!

Subscribe now and receive a special gift with your subscription.

See content on this topic

What is the difference between retention and loyalty, and between customer-centric and relationship-centric business models? How exactly can one monetize customer experience? Michael Ruckman answers these questions and more…

Michael Ruckman, President & CEO of Senteo talks about Customer Contacts, Experiences, and Journeys in this fast moving presentation from the MECS+R Congress in 2021 in Dubai.

Related Articles

Frontline Trainings

Front Line Sales Training & Development

Sales training for front line along with basic development and coaching principles for line management.

Master Class

Workshop

Experiential Branding & Communications – Improving Brand Integration Through Emotional Engagement

Understanding branding and communications from the standpoint of emotional engagement and building relevant and meaningful dialogue with customers.

Master Class

Workshop

Designing Experiential Customer Environments (Physical & Digital)

This course covers a complete view of customer touch points (both physical and virtual) and a unique model for standardizing and managing customer contact models across channels including approaches for customer feedback, quality management, and migration.

Management Trainings

Experiential Innovation & Relationship-Centric Business Design

Understand how the innovation process changes moving from functionality and channel design to a process focused on creating value for customers.

New

Online Course

Understanding Brand & Communications

Experiential Branding & Communications – Improving Brand Integration Through Emotional Engagement.

$195 One-Time Charge

Online Course

Understanding Customer Touch Points

This course covers a complete view of customer touch points (both physical and virtual) and a unique model for standardizing and managing customer contact models across channels.

$195 One-Time Charge

Master Class

Workshop

Using Customer-Oriented Analytics & Behavioral Scenarios to Improve Business Performance

Understand the value of a customer-oriented analytics package and how behavioral scenarios can be used to improve profitability through influencing behavior and usage.

Master Class

Workshop

Understanding Game Dynamics & Applying Gamification to Drive Customer / Employee Engagement & Loyalty

To understand the principles of game dynamics and learn how to effectively use the elements of gamification in business: to involve customers, employees and contractors in the process.

Master Class

Workshop

Experiential Branding & Communications – Improving Brand Integration Through Emotional Engagement

Understanding branding and communications from the standpoint of emotional engagement and building relevant and meaningful dialogue with customers.

Master Class

Workshop

Designing Experiential Customer Environments (Physical & Digital)

This course covers a complete view of customer touch points (both physical and virtual) and a unique model for standardizing and managing customer contact models across channels including approaches for customer feedback, quality management, and migration.

New

Online Course

Understanding Brand & Communications

Experiential Branding & Communications – Improving Brand Integration Through Emotional Engagement.

$195 One-Time Charge

Online Course

Understanding Customer Touch Points

This course covers a complete view of customer touch points (both physical and virtual) and a unique model for standardizing and managing customer contact models across channels.

$195 One-Time Charge

In a recent episode of the Escaping the Drift podcast, host John Gafford sat down with Michael Ruckman, founder and CEO of Centeo, to explore how artificial intelligence is reshaping business—and why organizational transformation must keep pace

Go Back

Go Back

Leave a Reply

You must be logged in to post a comment.